Model Selection via Custom Metrics

This AI Accelerator demonstrates how one can leverage DataRobot's python client to extract predictions, compute custom metrics, and sort their DataRobot models accordingly.

Build with Free TrialOverview

When it comes to evaluating machine learning model performance, DataRobot provides many of the standard metrics out-of-the box, either on the Leaderboard or as a model insight. However, depending on the industry, you may need to sort the Leaderboard by a specific metric that is not natively supported by DataRobot, or by return-on-investment (ROI). To help make this process easier, this notebook outlines a way to accomplish this leveraging DataRobot’s Python client for a supervised, binary classification problem.

This notebook outlines the following steps:

- Setup: import libraries and connect to DataRobot

- Build models with Autopilot

- Retrieve predictions and actuals

- Sort models by Brier Skill Score (BSS)

- Sort models by Rate@Top1%

- Sort models by ROI

Setup

First, import the necessary packages and set up the connection to the DataRobot platform.

Import libraries

In [1]:

from typing import Callable, List

from adjustText import adjust_text

import datarobot as dr

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from sklearn.metrics import brier_score_loss

print(f"DataRobot version: {dr.__version__}")DataRobot version: 3.0.2

Connect to DataRobot

Read more about different options for connecting to DataRobot from the client.

In [2]:

DATAROBOT_ENDPOINT = "https://app.datarobot.com/api/v2"

# The URL may vary depending on your hosting preference, the above example is for DataRobot Managed AI Cloud

DATAROBOT_API_TOKEN = "<INSERT YOUR DataRobot API Token>"

# The API Token can be found by click the avatar icon and then </> Developer Tools

client = dr.Client(

token=DATAROBOT_API_TOKEN,

endpoint=DATAROBOT_ENDPOINT,

user_agent_suffix="AIA-AE-CM-61", # Optional but helps DataRobot improve this workflow

)

dr.client._global_client = clientOut [2]:

<datarobot.rest.RESTClientObject at 0x10ddda4c0>

Import data

Next, load the following dataset from an Anti-Money Laundering (AML) example into memory. In this dataset, the unit of analysis is an individual alert and the target is binary, indicating if the alert resulted in a Suspicious Activity Report (SAR). SARs take time and money for AML compliance teams to file so being able to identify which alerts to focus (or not focus) on can result in millions of dollars saved per year.

In terms of bringing the dataset into DataRobot, you’ll use dr.Project.create(). While this isn’t the only way, having data already loaded into memory gives you the ability to easily match your predictions back to the actuals – a necessary step for computing metrics outside of DataRobot.

Define parameters

In [2]:

# Defining dataset and target

dataset_location = (

"https://s3.amazonaws.com/datarobot-use-case-datasets/DR_Demo_AML_Alert_train.csv"

)

target = "SAR"

# Load dataset

df = pd.read_csv(dataset_location)

dfOut [3]:

| 0 | 1 | 2 | 3 | 4 | … | 9995 | 9996 | 9997 | 9998 | 9999 | |

| ALERT | 1 | 1 | 1 | 1 | 1 | … | 1 | 1 | 1 | 1 | 1 |

| SAR | 0 | 0 | 0 | 0 | 0 | … | 0 | 0 | 0 | 0 | 0 |

| kycRiskScore | 3 | 2 | 1 | 0 | 1 | … | 2 | 2 | 0 | 1 | 2 |

| income | 110300 | 107800 | 74000 | 57700 | 59800 | … | 65000 | 37800 | 15000 | NaN | 160700 |

| tenureMonths | 5 | 6 | 13 | 1 | 3 | … | 18 | 135 | 3 | 42 | 21 |

| creditScore | 757 | 715 | 751 | 659 | 709 | … | 699 | 686 | 645 | 701 | 726 |

| state | PA | NY | MA | NJ | PA | … | PA | MA | MA | NY | NY |

| nbrPurchases90d | 10 | 22 | 7 | 14 | 54 | … | 40 | 3 | 5 | 7 | 2 |

| avgTxnSize90d | 153.8 | 1.59 | 57.64 | 29.52 | 115.77 | … | 4.47 | 9.9 | 241.34 | 60.73 | 17.58 |

| totalSpend90d | 1538 | 34.98 | 403.48 | 413.28 | 6251.58 | … | 178.8 | 29.7 | 1206.7 | 425.11 | 35.16 |

| … | … | … | … | … | … | … | … | … | … | … | … |

| indCustReqRefund90d | 1 | 1 | 1 | 1 | 1 | … | 1 | 1 | 1 | 1 | 1 |

| totalRefundsToCust90d | 45.82 | 67.4 | 450.69 | 71.43 | 2731.39 | … | 49.92 | 50.18 | 33.27 | 34.18 | 2830.21 |

| nbrPaymentsCashLike90d | 5 | 0 | 0 | 0 | 3 | … | 0 | 0 | 0 | 0 | 4 |

| maxRevolveLine | 6000 | 10000 | 10000 | 8000 | 7000 | … | 9000 | 10000 | 10000 | 7000 | 8000 |

| indOwnsHome | 0 | 1 | 0 | 1 | 1 | … | 1 | 0 | 0 | 0 | 0 |

| nbrInquiries1y | 3 | 3 | 3 | 5 | 1 | … | 4 | 1 | 2 | 1 | 2 |

| nbrCollections3y | 0 | 0 | 0 | 0 | 0 | … | 0 | 0 | 0 | 0 | 0 |

| nbrWebLogins90d | 6 | 87 | 6 | 7 | 8 | … | 11 | 5 | 10 | 6 | 12 |

| nbrPointRed90d | 1 | 0 | 0 | 2 | 1 | … | 1 | 1 | 0 | 0 | 1 |

| PEP | 0 | 0 | 0 | 0 | 0 | … | 0 | 0 | 0 | 0 | 0 |

Modeling

Create a project

In[4]:

project = dr.Project.create(sourcedata=df, project_name="Custom Metrics")

projectOut[4]:

Project(Custom Metrics)Run Autopilot

After creating a project, you can begin building models using DataRobot’s default modeling mode. Note that this is just the default setting, and you can generate more models by specifying one of the other modeling modes.

In [5]:

# Run models

project.analyze_and_model(

target=target,

worker_count=-1, # Setting the worker count to -1 will ensure that you use the max available workers for your account

max_wait=600,

advanced_options=dr.AdvancedOptions(

prepare_model_for_deployment=False

), # Will speed up modeling process

)

# Wait for them to complete

project.wait_for_autopilot()In progress: 9, queued: 0 (waited: 0s)

In progress: 9, queued: 0 (waited: 0s)

In progress: 9, queued: 0 (waited: 1s)

In progress: 9, queued: 0 (waited: 2s)

In progress: 9, queued: 0 (waited: 3s)

In progress: 9, queued: 0 (waited: 5s)

In progress: 9, queued: 0 (waited: 9s)

In progress: 9, queued: 0 (waited: 16s)

In progress: 9, queued: 0 (waited: 29s)

In progress: 6, queued: 0 (waited: 49s)

In progress: 16, queued: 0 (waited: 70s)

In progress: 14, queued: 0 (waited: 90s)

In progress: 6, queued: 0 (waited: 110s)

In progress: 1, queued: 0 (waited: 131s)

In progress: 0, queued: 0 (waited: 151s)Retrieve models

In [6]:

# List trained models

models = project.get_models()

print(f"Number of models built for this dataset: {len(models)}")

modelsNumber of models built for this dataset: 9

Out[6]:

[Model('RandomForest Classifier (Gini)'),

Model('eXtreme Gradient Boosted Trees Classifier with Early Stopping'),

Model('RuleFit Classifier'),

Model('Light Gradient Boosted Trees Classifier with Early Stopping'),

Model('Generalized Additive2 Model'),

Model('Light Gradient Boosting on ElasticNet Predictions '),

Model('Keras Slim Residual Neural Network Classifier using Training Schedule (1 Layer: 64 Units)'),

Model('Elastic-Net Classifier (L2 / Binomial Deviance)'),

Model('Elastic-Net Classifier (mixing alpha=0.5 / Binomial Deviance)')]Get predictions and actuals

In order to compute metrics manually, you need both the predictions and the actuals (i.e., the target’s actual values) associated with those predictions. To extract the former, use datarobot.models.Model.request_training_predictions() and for the latter, simply join the actuals from the dataset you have in memory based on the provided “row_id” by DataRobot. Because the predictions for each model will be different, you can save these as new attributes to the model object (below has a convenient function to add them for you). Note that this is just one way to do this. If you pull the models again via datarobot.models.Project.get_models() and overwrite your list of models, you’ll need to re-add the desired information to the Model objects.

In [7]:

# Helper function to get the out-of-sample predictions for a given model

def request_training_predictions(models: List[dr.models.model.Model], data_subset: str):

"""

Requests (and waits) out-of-sample predictions for a batch of models

Parameters

----------

models : List of DataRobot models

data_subset: string indicating data subset (see datarobot.enums.DATA_SUBSET)

"""

# Request predictions

jobs = []

for model in models:

try:

jobs.append(model.request_training_predictions(data_partition))

except:

pass

# Wait

jobs = [x.wait_for_completion(max_wait=60 * 60 * 24) for x in jobs]

def adds_oos_predictions_to_model(

model: dr.models.model.Model,

target_series: pd.Series,

data_subset: str,

):

"""

Adds the out-of-sample predictions (and relevant information) for a data subset from a model to that model as attributes

(assumes this is a binary project type)

Parameters

----------

model : DataRobot model

target_series: Binary target values for the dataset with the respective row ID as the index

data_subset: string indicating data subset (see datarobot.enums.DATA_SUBSET)

"""

# Get project object

project = dr.Project.get(model.project_id)

# Asserting target type is met

assert (

project.target_type == "Binary"

), "This function expects a binary classification project type!"

# Request or gather predictions

try:

training_predict_job = model.request_training_predictions(data_subset)

training_predictions = training_predict_job.get_result_when_complete(

max_wait=60 * 60 * 24

)

except dr.errors.ClientError:

training_predictions = [

tp

for tp in dr.TrainingPredictions.list(project.id)

if tp.model_id == model.id and tp.data_subset == data_subset

][0]

# Get as dataframe

preds = training_predictions.get_all_as_dataframe()

# Gather predictions and join actuals

preds = preds.set_index("row_id")

preds = preds.join(target_series)

# Define positive class (True / False is stored as float)

if isinstance(project.positive_class, str):

positive_class = project.positive_class

else:

positive_class = float(project.positive_class)

# Save information

model.__y_prob = preds[f"class_{positive_class}"].values

model.__y_true = preds[target].values

model.__partition_id = preds["partition_id"].values

model.__row_id = preds.indexIn [8]:

# Unlock the holdout to be used for analysis

project.unlock_holdout()

# Repull models so that holdout metric values are filled in

models = project.get_models()

# Specify the data partition

data_partition = dr.enums.DATA_SUBSET.VALIDATION_AND_HOLDOUT

# Request the out-of-sample predictions

request_training_predictions(models=models, data_subset=data_partition)In [9]:

# Add this information to your list of models as attributes

for model in models:

adds_oos_predictions_to_model(

model=model,

target_series=df[target],

data_subset=data_partition,

)

# Check one of them

print(f"Probabilities: {models[0].__y_prob}")

print(f"Target: {models[0].__y_true}")

print(f"Partition: {models[0].__partition_id}")

print(f"Row: {models[0].__row_id}")Probabilities: [0.250285 0.21784128 0. ... 0.0024568 0.00067236 0. ]

Target: [0 0 0 ... 0 0 0]

Partition: ['Holdout' 'Holdout' 'Holdout' ... 'Holdout' 'Holdout' 'Holdout']

Row: Int64Index([ 1, 2, 5, 6, 9, 10, 12, 17, 19, 22,

...

9976, 9985, 9986, 9988, 9989, 9990, 9991, 9992, 9994, 9995],

dtype='int64', name='row_id', length=3600)Sort models by Brier Skill Score (BSS)

Now that you have the necessary data, you can begin evaluating the DataRobot models using whatever metrics you’d like. Below is an example using a metric not given to you out-of-the-box by DataRobot, Brier Skill Score), with the help of sklearn’s brier_score_loss() function. Brier Score is similar to Log Loss but is strictly bounded between [0,1] (Log Loss is bounded between [0,+∞)).

Brier Skill Score is an extension of the Brier Score where you compare the Brier Score of a candidate model to a reference model’s to understand how much better (or worse) a model is relatively. For defining the reference model, a common practice is to use the positive class event rate from the dataset you’re evaluating.

In [10]:

# Define the BSS function

def brier_skill_score(

y_true: np.array, y_prob_candidate: np.array, y_prob_reference: np.array, **kwargs

) -> float:

"""

Computes Brier Skill Score (the larger the better)

Parameters

----------

y_true: true labels

y_prob_candidate: probability predictions from a candidate model

y_prob_reference: probability predictions from a reference model

**kwargs: additional arguments to pass to `brier_score_loss()`

Returns

-------

Brier Skill Score value

References

-------

https://en.wikipedia.org/wiki/Brier_score#Brier_Skill_Score_(BSS)

"""

# Compute Brier Scores

bs_candidate = brier_score_loss(y_true=y_true, y_prob=y_prob_candidate, **kwargs)

bs_reference = brier_score_loss(y_true=y_true, y_prob=y_prob_reference, **kwargs)

return 1 - bs_candidate / bs_referenceIn [11]:

# Reference model predictions (the event rate propagated forward)

baseline = np.mean(models[0].__y_true == project.positive_class)

baselineOut [11]:

0.10277777777777777

In [12]:

# Example

brier_skill_score(

y_true=models[0].__y_true,

y_prob_candidate=models[0].__y_prob,

y_prob_reference=np.repeat(baseline, len(models[0].__y_true)),

pos_label=project.positive_class,

)

Out [12]:

0.43302782027907316

In [13]:

# An example of how a model stores its performance metric information

models[0].metrics

Out [13]:

{'AUC': {'validation': 0.94542,

'crossValidation': 0.9446899999999999,

'holdout': 0.95553,

'training': None,

'backtestingScores': None,

'backtesting': None},

'Area Under PR Curve': {'validation': 0.59093,

'crossValidation': 0.606878,

'holdout': 0.67187,

'training': None,

'backtestingScores': None,

'backtesting': None},

'FVE Binomial': {'validation': 0.51133,

'crossValidation': 0.5136839999999999,

'holdout': 0.54902,

'training': None,

'backtestingScores': None,

'backtesting': None},

'Gini Norm': {'validation': 0.89084,

'crossValidation': 0.8893800000000001,

'holdout': 0.91106,

'training': None,

'backtestingScores': None,

'backtesting': None},

'Kolmogorov-Smirnov': {'validation': 0.83426,

'crossValidation': 0.8329359999999999,

'holdout': 0.83389,

'training': None,

'backtestingScores': None,

'backtesting': None},

'LogLoss': {'validation': 0.16153,

'crossValidation': 0.16074799999999997,

'holdout': 0.14956,

'training': None,

'backtestingScores': None,

'backtesting': None},

'Max MCC': {'validation': 0.58339,

'crossValidation': 0.586418,

'holdout': 0.60468,

'training': None,

'backtestingScores': None,

'backtesting': None},

'RMSE': {'validation': 0.23521,

'crossValidation': 0.234088,

'holdout': 0.22327,

'training': None,

'backtestingScores': None,

'backtesting': None},

'Rate@Top10%': {'validation': 0.575,

'crossValidation': 0.56125,

'holdout': 0.64,

'training': None,

'backtestingScores': None,

'backtesting': None},

'Rate@Top5%': {'validation': 0.6625,

'crossValidation': 0.72,

'holdout': 0.81,

'training': None,

'backtestingScores': None,

'backtesting': None},

'Rate@TopTenth%': {'validation': 0.5,

'crossValidation': 0.7,

'holdout': 1.0,

'training': None,

'backtestingScores': None,

'backtesting': None}}

In [14]:

# Save the BSS score for each model in the same way

for model in models:

# Compute for each partition

valid_score = brier_skill_score(

y_true=model.__y_true[model.__partition_id == "0.0"],

y_prob_candidate=model.__y_prob[model.__partition_id == "0.0"],

y_prob_reference=np.repeat(

baseline, len(model.__y_true[model.__partition_id == "0.0"])

),

pos_label=project.positive_class,

)

holdout_score = brier_skill_score(

y_true=model.__y_true[model.__partition_id == "Holdout"],

y_prob_candidate=model.__y_prob[model.__partition_id == "Holdout"],

y_prob_reference=np.repeat(

baseline, len(model.__y_true[model.__partition_id == "Holdout"])

),

pos_label=project.positive_class,

)

# Create new metrics entry (with the same format)

model.metrics["BSS"] = {

"validation": valid_score,

"crossValidation": None,

"holdout": holdout_score,

"training": None,

"backtestingScores": None,

"backtesting": None,

}

print(

f"{model.model_type}: {round(model.metrics['BSS']['validation'], 4)}, {round(model.metrics['BSS']['holdout'], 4)}"

)RandomForest Classifier (Gini): 0.3986, 0.4604

eXtreme Gradient Boosted Trees Classifier with Early Stopping: 0.3985, 0.4692

RuleFit Classifier: 0.3623, 0.4383

Light Gradient Boosted Trees Classifier with Early Stopping: 0.3795, 0.4557

Generalized Additive2 Model: 0.3707, 0.4342

Light Gradient Boosting on ElasticNet Predictions : 0.3494, 0.4357

Keras Slim Residual Neural Network Classifier using Training Schedule (1 Layer: 64 Units): 0.3484, 0.3853

Elastic-Net Classifier (L2 / Binomial Deviance): 0.293, 0.2534

Elastic-Net Classifier (mixing alpha=0.5 / Binomial Deviance): 0.2904, 0.259In [15]:

# Can inspect BSS alongside DataRobot's metrics

pd.DataFrame(model.metrics).T.dropna(axis=1)Out[15]:

| validation | holdout | |

|---|---|---|

| AUC | 0.92564 | 0.922840 |

| Area Under PR Curve | 0.54531 | 0.513740 |

| FVE Binomial | 0.35798 | 0.340810 |

| Gini Norm | 0.85128 | 0.845680 |

| Kolmogorov-Smirnov | 0.77206 | 0.772760 |

| LogLoss | 0.21222 | 0.218600 |

| Max MCC | 0.54830 | 0.538350 |

| RMSE | 0.25550 | 0.261650 |

| Rate@Top10% | 0.49375 | 0.485000 |

| Rate@Top5% | 0.63750 | 0.540000 |

| Rate@TopTenth% | 1.00000 | 1.000000 |

| BSS | 0.29041 | 0.259016 |

In [16]:

# Sort the Leaderboard

# Note that you sort by the valdiation only to preserve the integrity of the holdout data

models_sorted_by_bss = sorted(

models, key=lambda x: x.metrics["BSS"]["validation"], reverse=True

)

models_sorted_by_bssOut [16]:

[Model('RandomForest Classifier (Gini)'),

Model('eXtreme Gradient Boosted Trees Classifier with Early Stopping'),

Model('Light Gradient Boosted Trees Classifier with Early Stopping'),

Model('Generalized Additive2 Model'),

Model('RuleFit Classifier'),

Model('Light Gradient Boosting on ElasticNet Predictions '),

Model('Keras Slim Residual Neural Network Classifier using Training Schedule (1 Layer: 64 Units)'),

Model('Elastic-Net Classifier (L2 / Binomial Deviance)'),

Model('Elastic-Net Classifier (mixing alpha=0.5 / Binomial Deviance)')]Sort models by Rate@Top1%

Now that you’ve seen an example of a metric not included in DataRobot, let’s look at another example where you take an existing metric and expand on it. DataRobot’s Rate@Top10%, Rate@Top5%, and Rate@TopTenth% metrics are extremely useful for understanding how many events a model is capturing (in this case SAR alerts) in the highest predictions. Oftentimes, 10%, 5%, and 0.1% are sufficient, but some use cases may require computing different percentages. To this end, below is a function to compute this statistic for any percentage.

In [17]:

# Define Rate@TopX% function

def rate_at_top_x(

y_true: np.array, y_prob: np.array, percentage: float, positive_class: str

) -> float:

"""

Computes DataRobot's Rate@TopX% metric for any percentage

Parameters

----------

y_true: true labels

y_prob: probability predictions from a model

percentage: percentage to use for the rate metric

positive_class: event class associated with model

Returns

-------

Rate@TopX% value

References

-------

https://app.datarobot.com/docs/modeling/reference/model-detail/opt-metric.html#ratetop10-ratetop5-ratetoptenth

"""

# Ensure percentage is in bounds

assert 0 <= percentage <= 100, "Percentage needs to be [0, 100]"

# Make boolean

actuals_mask = y_true == positive_class

# Find top X predictions

top_preds_mask = y_prob >= np.percentile(y_prob, 100 - percentage)

# To avoid dividing by 0

if top_preds_mask.sum() == 0:

return 0.0

# Compute rate

return (actuals_mask * top_preds_mask).sum() / top_preds_mask.sum()In [18]:

# Verify by comparing your metric back to DataRobot on the validation partition

for i in [10, 5, 0.1]:

# Compute for each partition

valid_value = rate_at_top_x(

y_true=models[0].__y_true[models[0].__partition_id == "0.0"],

y_prob=models[0].__y_prob[models[0].__partition_id == "0.0"],

percentage=i,

positive_class=project.positive_class,

)

holdout_value = rate_at_top_x(

y_true=models[0].__y_true[models[0].__partition_id == "Holdout"],

y_prob=models[0].__y_prob[models[0].__partition_id == "Holdout"],

percentage=i,

positive_class=project.positive_class,

)

# DataRobot's value

if i == 0.1:

dr_valid_value = models[0].metrics["Rate@TopTenth%"]["validation"]

dr_holdout_value = models[0].metrics["Rate@TopTenth%"]["holdout"]

else:

dr_valid_value = models[0].metrics[f"Rate@Top{i}%"]["validation"]

dr_holdout_value = models[0].metrics[f"Rate@Top{i}%"]["holdout"]

print(

f"Computed Rate@Top{i}%: {round(valid_value, 4)}, {round(holdout_value, 4)} | DataRobot's: {dr_valid_value}, {dr_holdout_value}"

)Computed Rate@Top10%: 0.575, 0.64 | DataRobot's: 0.575, 0.64

Computed Rate@Top5%: 0.6625, 0.81 | DataRobot's: 0.6625, 0.81

Computed Rate@Top0.1%: 0.5, 1.0 | DataRobot's: 0.5, 1.0In [19]:

# Compute and save the Rate@Top1%

for model in models:

# Compute for each partition

valid_score = rate_at_top_x(

y_true=model.__y_true[model.__partition_id == "0.0"],

y_prob=model.__y_prob[model.__partition_id == "0.0"],

percentage=1,

positive_class=project.positive_class,

)

holdout_score = rate_at_top_x(

y_true=model.__y_true[model.__partition_id == "Holdout"],

y_prob=model.__y_prob[model.__partition_id == "Holdout"],

percentage=1,

positive_class=project.positive_class,

)

# Create new metrics entry (with same format)

model.metrics["Rate@Top1%"] = {

"validation": valid_score,

"crossValidation": None,

"holdout": holdout_score,

"training": None,

"backtestingScores": None,

"backtesting": None,

}

print(

f"{model.model_type}: {round(model.metrics['Rate@Top1%']['validation'], 4)}, {round(model.metrics['Rate@Top1%']['holdout'], 4)}"

)RandomForest Classifier (Gini): 0.75, 0.9

eXtreme Gradient Boosted Trees Classifier with Early Stopping: 0.8125, 0.7

RuleFit Classifier: 0.75, 0.8

Light Gradient Boosted Trees Classifier with Early Stopping: 0.75, 0.75

Generalized Additive2 Model: 0.8125, 0.75

Light Gradient Boosting on ElasticNet Predictions : 0.8125, 0.75

Keras Slim Residual Neural Network Classifier using Training Schedule (1 Layer: 64 Units): 0.8125, 0.85

Elastic-Net Classifier (L2 / Binomial Deviance): 0.75, 0.8

Elastic-Net Classifier (mixing alpha=0.5 / Binomial Deviance): 0.75, 0.75In [20]:

# Sort the leaderboard

models_sorted_by_rate_at_top1 = sorted(

models, key=lambda x: x.metrics["Rate@Top1%"]["validation"], reverse=True

)

models_sorted_by_rate_at_top1Out [20]:

[Model('eXtreme Gradient Boosted Trees Classifier with Early Stopping'),

Model('Generalized Additive2 Model'),

Model('Light Gradient Boosting on ElasticNet Predictions '),

Model('Keras Slim Residual Neural Network Classifier using Training Schedule (1 Layer: 64 Units)'),

Model('RandomForest Classifier (Gini)'),

Model('RuleFit Classifier'),

Model('Light Gradient Boosted Trees Classifier with Early Stopping'),

Model('Elastic-Net Classifier (L2 / Binomial Deviance)'),

Model('Elastic-Net Classifier (mixing alpha=0.5 / Binomial Deviance)')]

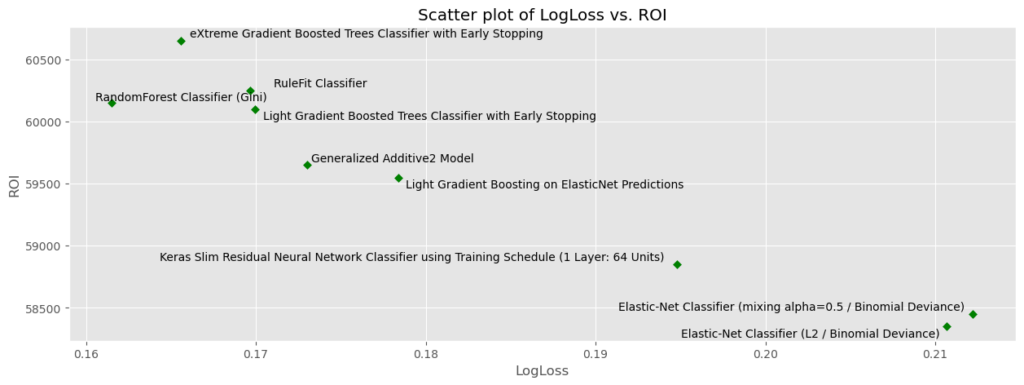

Sort models by ROI

While machine learning metrics like Brier Skill Score and Rate@TopX% are useful for understanding empirical prediction performance, they don’t easily map to business value. Although sometimes difficult, assigning the ROI of utilizing machine learning can be vital for use case adoption and model implementation. Here, you will explore a similar exercise as above but with computing a dollar figure rather than a machine learning metric. Since this is a binary classification problem, 4 possible outcomes exist:

- True positive (TP): The model correctly predicted that the alert would result in a SAR.

- True negative (TN): The model correctly predicted that the alert would not result in a SAR.

- False positive (FP): The model incorrectly predicted that the alert would result in a SAR.

- False negative (FN): The model incorrectly predicted that the alert would not result in a SAR.

For the sake of example, you can use the same cost estimates described here, which are:

- Cost of investigating an alert: -$50

- Cost of remediating a SAR that was not detected: -$200

Given that each alert costs -$50 to review and a financial institution explores each alert, one way to compute ROI is in terms of savings from using a model-based approach:

ROI = cost_with_model – cost_without_model

where

cost_with_model = -($50 * number of alerts flagged + $200 * number of SAR alerts missed) = -(50 * (TPs + FPs) + 200 * FNs)

cost_without_model = -$50 * all alerts

Note that in order to assign ROI to each model, you must first establish a threshold to apply to the predicted probabilities (so that a model can determine if an alert is SAR-worthy or not). Finding this threshold generally involves optimizing some sort of metric (e.g., F1-score). Here, you’ll use the validation partition to find the threshold that maximizes ROI and then use that threshold to determine the ROI on the holdout partition. Each of these values will be recorded as done previously under the “metrics” attribute within the model object.

In [21]:

# Helpers for finding the best threshold according to a supplied payoff matrix

def compute_total_profit(

payoff_matrix: dr.models.PayoffMatrix,

true_positive_count: int,

true_negative_count: int,

false_positive_count: int,

false_negative_count: int,

) -> float:

"""

Computes a value representing total profit

Parameters

----------

payoff_matrix: a DataRobot payoff matrix

true_positive_count: number of true positives

true_negative_count: number of true negatives

false_positive_count: number of false positives

false_negative_count: number of false negatives

Returns

-------

A value representing the total profit

"""

# Compute values

tp_total = payoff_matrix.true_positive_value * true_positive_count

tn_total = payoff_matrix.true_negative_value * true_negative_count

fp_total = payoff_matrix.false_positive_value * false_positive_count

fn_total = payoff_matrix.false_negative_value * false_negative_count

return tp_total + tn_total + fp_total + fn_total

def optimize_thresholds_by_total_profit(

model: dr.models.model.Model,

profit_function: Callable,

payoff_matrix: dr.models.PayoffMatrix,

data_source: str,

) -> tuple:

"""

Find the threshold that maximizes the value return by profit function in a data partition

Parameters

----------

model : DataRobot model

profit_function: function to compute profit with (should return a float)

payoff_matrix: a DataRobot payoff matrix

data_source: string indicating data source (see datarobot.enums.CHART_DATA_SOURCE)

Returns

-------

Threshold that maximizes total profit and the respective total profit value

"""

# Leveraging the pre-computed thresholds from DataRobot

thresholds = model.get_roc_curve(source=data_source).roc_points

# Cycle through each threshold

results = {}

for i in range(len(thresholds)):

# Assign counts

true_positive_count = thresholds[i]["true_positive_score"]

true_negative_count = thresholds[i]["true_negative_score"]

false_positive_count = thresholds[i]["false_positive_score"]

false_negative_count = thresholds[i]["false_negative_score"]

# Pass the confusion matrix counts to the ROI function

profit = profit_function(

payoff_matrix=payoff_matrix,

true_positive_count=true_positive_count,

true_negative_count=true_negative_count,

false_positive_count=false_positive_count,

false_negative_count=false_negative_count,

)

# Save results

results[thresholds[i]["threshold"]] = profit

# Find threshold with maximum profit

best_threshold = max(results, key=results.get)

# Return threshold and profit value

return best_threshold, results[best_threshold]In [22]:

# Create payoff matrix (note that negative values represent costs)

# This can be viewed in the UI

payoff_matrix = dr.models.PayoffMatrix.create(

project_id=project.id,

name="AML Costs",

true_positive_value=-50,

true_negative_value=0,

false_positive_value=-50,

false_negative_value=-200,

)Use the snippet below to run through each model, find the threshold that maximizes total profit on validation partition, apply it to the holdout, and save results.

In [23]:

for model in models:

# Compute the threshold to use

threshold, valid_profit = optimize_thresholds_by_total_profit(

model=model,

profit_function=compute_total_profit,

payoff_matrix=payoff_matrix,

data_source=dr.enums.CHART_DATA_SOURCE.VALIDATION,

)

# Apply threshold to holdout

holdout_info = model.get_roc_curve(

source=dr.enums.CHART_DATA_SOURCE.HOLDOUT

).estimate_threshold(threshold)

# Compute payoff on holdout

holdout_profit = compute_total_profit(

payoff_matrix=payoff_matrix,

true_positive_count=holdout_info["true_positive_score"],

true_negative_count=holdout_info["true_negative_score"],

false_positive_count=holdout_info["false_positive_score"],

false_negative_count=holdout_info["false_negative_score"],

)

# Create new metrics entry (with same format)

model.metrics["Total Profit"] = {

"validation": valid_profit,

"crossValidation": None,

"holdout": holdout_profit,

"training": None,

"backtestingScores": None,

"backtesting": None,

}

# Save threshold to the model

model.__best_threshold_by_total_profit = threshold

print(

f"{model.model_type} (threshold = {round(model.__best_threshold_by_total_profit, 2)}): {model.metrics['Total Profit']['validation']}, {model.metrics['Total Profit']['holdout']}"

)RandomForest Classifier (Gini) (threshold = 0.22): -19850.0, -24350.0

eXtreme Gradient Boosted Trees Classifier with Early Stopping (threshold = 0.18): -19350.0, -24400.0

RuleFit Classifier (threshold = 0.14): -19750.0, -24950.0

Light Gradient Boosted Trees Classifier with Early Stopping (threshold = 0.17): -19900.0, -24350.0

Generalized Additive2 Model (threshold = 0.12): -20350.0, -25600.0

Light Gradient Boosting on ElasticNet Predictions (threshold = 0.11): -20450.0, -25600.0

Keras Slim Residual Neural Network Classifier using Training Schedule (1 Layer: 64 Units) (threshold = 0.23): -21150.0, -26800.0

Elastic-Net Classifier (L2 / Binomial Deviance) (threshold = 0.16): -21650.0, -29000.0

Elastic-Net Classifier (mixing alpha=0.5 / Binomial Deviance) (threshold = 0.16): -21550.0, -29000.0In [24]:

# Now that we have the costs associated with the model, you can now compute ROI for this use case

n_alerts_valid = sum(model.__partition_id == "0.0")

n_alerts_holdout = sum(model.__partition_id == "Holdout")

cost_without_model_valid = -50 * n_alerts_valid

cost_without_model_holdout = -50 * n_alerts_holdout

# Now iterate through to compute the final ROI value

for model in models:

# Cost with model

cost_with_model_valid = model.metrics["Total Profit"]["validation"]

cost_with_model_holdout = model.metrics["Total Profit"]["holdout"]

# Compute savings (aka ROI)

valid_savings = cost_with_model_valid - cost_without_model_valid

holdout_savings = cost_with_model_valid - cost_without_model_holdout

# Create new metrics entry (with same format)

model.metrics["ROI"] = {

"validation": valid_savings,

"crossValidation": None,

"holdout": holdout_savings,

"training": None,

"backtestingScores": None,

"backtesting": None,

}

print(

f"{model.model_type} (threshold = {round(model.__best_threshold_by_total_profit, 2)}): {model.metrics['ROI']['validation']}, {model.metrics['ROI']['holdout']}"

)RandomForest Classifier (Gini) (threshold = 0.22): 60150.0, 80150.0

eXtreme Gradient Boosted Trees Classifier with Early Stopping (threshold = 0.18): 60650.0, 80650.0

RuleFit Classifier (threshold = 0.14): 60250.0, 80250.0

Light Gradient Boosted Trees Classifier with Early Stopping (threshold = 0.17): 60100.0, 80100.0

Generalized Additive2 Model (threshold = 0.12): 59650.0, 79650.0

Light Gradient Boosting on ElasticNet Predictions (threshold = 0.11): 59550.0, 79550.0

Keras Slim Residual Neural Network Classifier using Training Schedule (1 Layer: 64 Units) (threshold = 0.23): 58850.0, 78850.0

Elastic-Net Classifier (L2 / Binomial Deviance) (threshold = 0.16): 58350.0, 78350.0

Elastic-Net Classifier (mixing alpha=0.5 / Binomial Deviance) (threshold = 0.16): 58450.0, 78450.0In [25]:

# Now sort the Leaderboard

models_sorted_by_roi = sorted(

models, key=lambda x: x.metrics["ROI"]["validation"], reverse=True

)

models_sorted_by_roiOut [25]:

[Model('eXtreme Gradient Boosted Trees Classifier with Early Stopping'),

Model('RuleFit Classifier'),

Model('RandomForest Classifier (Gini)'),

Model('Light Gradient Boosted Trees Classifier with Early Stopping'),

Model('Generalized Additive2 Model'),

Model('Light Gradient Boosting on ElasticNet Predictions '),

Model('Keras Slim Residual Neural Network Classifier using Training Schedule (1 Layer: 64 Units)'),

Model('Elastic-Net Classifier (mixing alpha=0.5 / Binomial Deviance)'),

Model('Elastic-Net Classifier (L2 / Binomial Deviance)')]Conclusion

In this notebook, you explored a way to evaluate DataRobot models using custom metrics. This example demonstrates the amount of flexibility and creativity that you can instill upon your model selection, whether that’s ranking DataRobot models according to a stakeholder metric of interest or by estimated ROI. Below shows the Leaderboard ranking for each of the computed metrics and some supporting visuals.

In [26]:

# Compare the various sorting options:

pd.DataFrame(

{

f"model_rank_{project.metric}": [x.model_type for x in models],

"model_rank_bss": [x.model_type for x in models_sorted_by_bss],

"model_rank_rate_at_top1": [

x.model_type for x in models_sorted_by_rate_at_top1

],

"model_rank_roi": [x.model_type for x in models_sorted_by_roi],

}

)Out [26]:

| model_rank_LogLoss | model_rank_bss | model_rank_rate_at_top1 | model_rank_roi | |

| 0 | RandomForest Classifier (Gini) | RandomForest Classifier (Gini) | eXtreme Gradient Boosted Trees Classifier with… | eXtreme Gradient Boosted Trees Classifier with… |

| 1 | eXtreme Gradient Boosted Trees Classifier with… | eXtreme Gradient Boosted Trees Classifier with… | Generalized Additive2 Model | RuleFit Classifier |

| 2 | RuleFit Classifier | Light Gradient Boosted Trees Classifier with E… | Light Gradient Boosting on ElasticNet Predicti… | RandomForest Classifier (Gini) |

| 3 | Light Gradient Boosted Trees Classifier with E… | Generalized Additive2 Model | Keras Slim Residual Neural Network Classifier … | Light Gradient Boosted Trees Classifier with E… |

| 4 | Generalized Additive2 Model | RuleFit Classifier | RandomForest Classifier (Gini) | Generalized Additive2 Model |

| 5 | Light Gradient Boosting on ElasticNet Predicti… | Light Gradient Boosting on ElasticNet Predicti… | RuleFit Classifier | Light Gradient Boosting on ElasticNet Predicti… |

| 6 | Keras Slim Residual Neural Network Classifier … | Keras Slim Residual Neural Network Classifier … | Light Gradient Boosted Trees Classifier with E… | Keras Slim Residual Neural Network Classifier … |

| 7 | Elastic-Net Classifier (L2 / Binomial Deviance) | Elastic-Net Classifier (L2 / Binomial Deviance) | Elastic-Net Classifier (L2 / Binomial Deviance) | Elastic-Net Classifier (mixing alpha=0.5 / Bin… |

| 8 | Elastic-Net Classifier (mixing alpha=0.5 / Bin… | Elastic-Net Classifier (mixing alpha=0.5 / Bin… | Elastic-Net Classifier (mixing alpha=0.5 / Bin… | Elastic-Net Classifier (L2 / Binomial Deviance) |

In [27]:

# Can inspect all new metrics alongside DataRobot's metrics

pd.DataFrame(model.metrics).T.dropna(axis=1)Out[27]:

| validation | holdout | |

|---|---|---|

| AUC | 0.92564 | 0.922840 |

| Area Under PR Curve | 0.54531 | 0.513740 |

| FVE Binomial | 0.35798 | 0.340810 |

| Gini Norm | 0.85128 | 0.845680 |

| Kolmogorov-Smirnov | 0.77206 | 0.772760 |

| LogLoss | 0.21222 | 0.218600 |

| Max MCC | 0.54830 | 0.538350 |

| RMSE | 0.25550 | 0.261650 |

| Rate@Top10% | 0.49375 | 0.485000 |

| Rate@Top5% | 0.63750 | 0.540000 |

| Rate@TopTenth% | 1.00000 | 1.000000 |

| BSS | 0.29041 | 0.259016 |

| Rate@Top1% | 0.75000 | 0.750000 |

| Total Profit | -21550.00000 | -29000.000000 |

| ROI | 58450.00000 | 78450.000000 |

In [28]:

# Add some visuals around these results

def prep_metric_data_for_plotting(

models: List[dr.models.model.Model], data_source: str

) -> pd.DataFrame:

"""

Organizing the metric data into a dataframe

Parameters

----------

models : List of DataRobot models

data_source: string indicating data source (see datarobot.enums.CHART_DATA_SOURCE)

Returns

-------

Dataframe of metrics with model info in the index

"""

# To save results

df_metrics = pd.DataFrame()

# Cycle through each model and save results

for model in models:

# Make into dataframe

tmp_df = pd.DataFrame(model.metrics).assign(

model_id=model.id, model_type=model.model_type

)

# Subset to requested data source

tmp_df = tmp_df.loc[tmp_df.index.isin([data_source])]

# Make model ID index

tmp_df = tmp_df.set_index(["model_id", "model_type"])

# Append

df_metrics = pd.concat([df_metrics, tmp_df])

return df_metrics

def scatter_plot(

df: pd.DataFrame,

x_axis_metric: str,

y_axis_metric: str,

label_as_model_type: bool,

**kwargs,

):

"""

Scatter plot of two metrics with model info annotated on the points

Parameters

----------

df: output from the function "prep_metric_data_for_plotting()"

x_axis_metric: name of metric to plot on x-axis

y_axis_metric: name of metric to plot on y-axis

label_as_model_type: whether to use the model_type as the label or the model ID

**kwargs: additional arguments to pass to plotting function

"""

# Make plot

df.plot.scatter(x_axis_metric, y_axis_metric, **kwargs)

# If true, use model type as label

# Else use model ID

if label_as_model_type:

labels = df.index.droplevel(-2)

else:

labels = df.index.droplevel(-1)

# Annotate each data point

x = df[x_axis_metric].values

y = df[y_axis_metric].values

ts = []

for i, txt in enumerate(labels):

ts.append(plt.text(x[i], y[i], txt))

# Space text labels out

adjust_text(ts, x=x, y=y)

plt.show()

In [29]:

# Create data for plotting

plot_data = prep_metric_data_for_plotting(

models=models, data_source=dr.enums.CHART_DATA_SOURCE.VALIDATION

)

plot_data

Out [29]:

| model_id | 63e157785d0bfd338104ba5a | 63e157785d0bfd338104ba5c | 63e157785d0bfd338104ba5b | 63e157785d0bfd338104ba58 | 63e157785d0bfd338104ba57 | 63e157785d0bfd338104ba59 | 63e157785d0bfd338104ba54 | 63e157785d0bfd338104ba55 | 63e157785d0bfd338104ba56 |

| model_type | RandomForest Classifier (Gini) | eXtreme Gradient Boosted Trees Classifier with Early Stopping | RuleFit Classifier | Light Gradient Boosted Trees Classifier with Early Stopping | Generalized Additive2 Model | Light Gradient Boosting on ElasticNet Predictions | Keras Slim Residual Neural Network Classifier using Training Schedule (1 Layer: 64 Units) | Elastic-Net Classifier (L2 / Binomial Deviance) | Elastic-Net Classifier (mixing alpha=0.5 / Binomial Deviance) |

| AUC | 0.94542 | 0.94675 | 0.94047 | 0.94252 | 0.94185 | 0.93912 | 0.93578 | 0.92361 | 0.92564 |

| Area Under PR Curve | 0.59093 | 0.59994 | 0.58264 | 0.58087 | 0.58339 | 0.59906 | 0.57099 | 0.5425 | 0.54531 |

| FVE Binomial | 0.51133 | 0.499 | 0.4867 | 0.48582 | 0.47659 | 0.46032 | 0.41071 | 0.36268 | 0.35798 |

| Gini Norm | 0.89084 | 0.8935 | 0.88094 | 0.88504 | 0.8837 | 0.87824 | 0.87156 | 0.84722 | 0.85128 |

| Kolmogorov-Smirnov | 0.83426 | 0.84192 | 0.83426 | 0.83374 | 0.8273 | 0.81736 | 0.77174 | 0.74037 | 0.77206 |

| LogLoss | 0.16153 | 0.1656 | 0.16967 | 0.16996 | 0.17301 | 0.17839 | 0.19478 | 0.21066 | 0.21222 |

| Max MCC | 0.58339 | 0.59765 | 0.58647 | 0.58868 | 0.57606 | 0.57852 | 0.55373 | 0.53528 | 0.5483 |

| RMSE | 0.23521 | 0.23524 | 0.24221 | 0.23891 | 0.24061 | 0.24465 | 0.24484 | 0.25503 | 0.2555 |

| Rate@Top10% | 0.575 | 0.55 | 0.55 | 0.55 | 0.54375 | 0.53125 | 0.54375 | 0.5125 | 0.49375 |

| Rate@Top5% | 0.6625 | 0.6625 | 0.6875 | 0.6625 | 0.7125 | 0.6625 | 0.625 | 0.5875 | 0.6375 |

| Rate@TopTenth% | 0.5 | 0.5 | 0.5 | 0.5 | 0 | 1 | 1 | 1 | 1 |

| BSS | 0.398631 | 0.398484 | 0.362299 | 0.379528 | 0.370673 | 0.349385 | 0.348352 | 0.292966 | 0.29041 |

| Rate@Top1% | 0.75 | 0.8125 | 0.75 | 0.75 | 0.8125 | 0.8125 | 0.8125 | 0.75 | 0.75 |

| Total Profit | -19850 | -19350 | -19750 | -19900 | -20350 | -20450 | -21150 | -21650 | -21550 |

| ROI | 60150 | 60650 | 60250 | 60100 | 59650 | 59550 | 58850 | 58350 | 58450 |

In [30]:

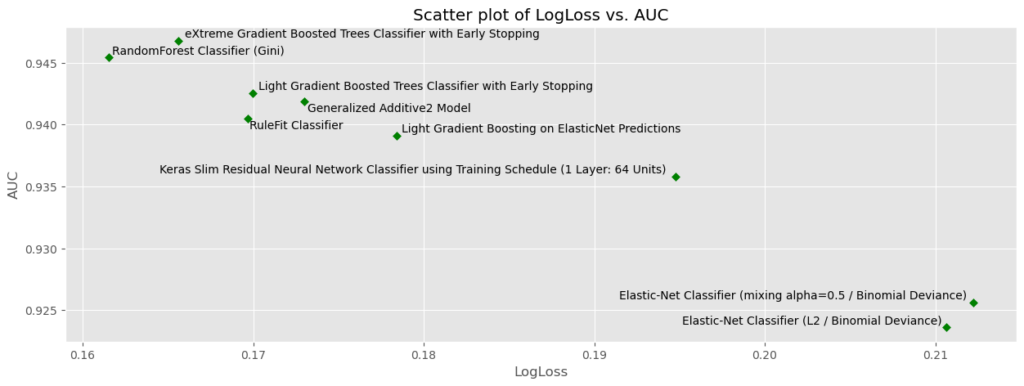

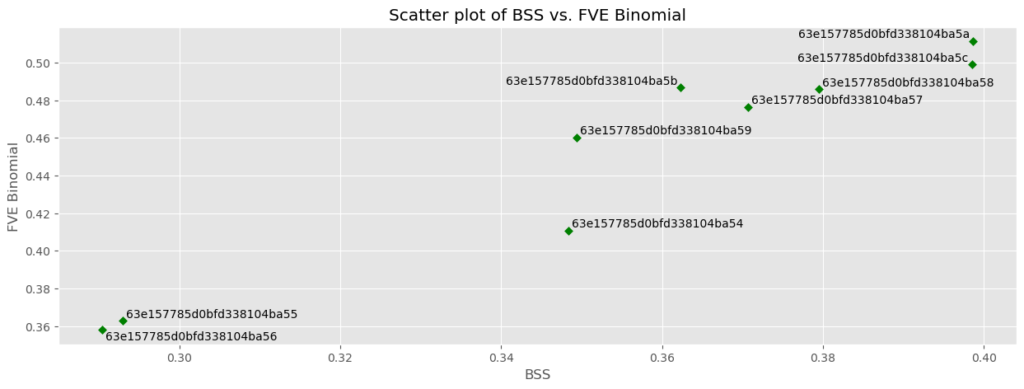

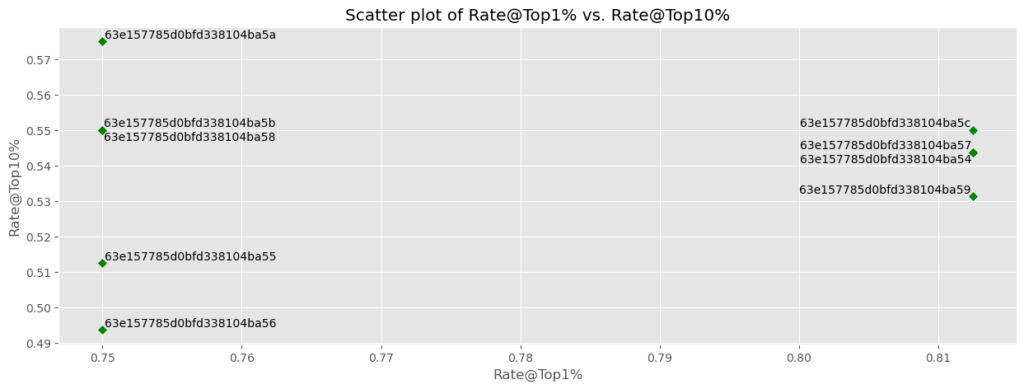

# Make some plots

metrics_to_plot = pd.DataFrame(

{

"x_axis_metrics": ["LogLoss", "BSS", "Rate@Top1%", "LogLoss"],

"y_axis_metrics": ["AUC", "FVE Binomial", "Rate@Top10%", "ROI"],

"label_as_model_type": [True, False, False, True],

}

)

# Cycle through each combination

plt.style.use("ggplot")

for i in range(metrics_to_plot.shape[0]):

# Set metrics

x_axis_metric = metrics_to_plot["x_axis_metrics"].iloc[i]

y_axis_metric = metrics_to_plot["y_axis_metrics"].iloc[i]

label_as_model_type = metrics_to_plot["label_as_model_type"].iloc[i]

# Make plot

scatter_plot(

df=plot_data,

x_axis_metric=x_axis_metric,

y_axis_metric=y_axis_metric,

label_as_model_type=label_as_model_type,

figsize=(15, 5),

color="green",

marker="D",

s=25,

title=f"Scatter plot of {x_axis_metric} vs. {y_axis_metric}",

xlabel=x_axis_metric,

ylabel=y_axis_metric,

)

Explore more AI Accelerators

-

HorizontalObject Classification on Video with DataRobot Visual AI

This AI Accelerator demonstrates how deep learning model trained and deployed with DataRobot platform can be used for object detection on the video stream (detection if person in front of camera wears glasses).

Learn More -

HorizontalPrediction Intervals via Conformal Inference

This AI Accelerator demonstrates various ways for generating prediction intervals for any DataRobot model. The methods presented here are rooted in the area of conformal inference (also known as conformal prediction).

Learn More -

HorizontalReinforcement Learning in DataRobot

In this notebook, we implement a very simple model based on the Q-learning algorithm. This notebook is intended to show a basic form of RL that doesn't require a deep understanding of neural networks or advanced mathematics and how one might deploy such a model in DataRobot.

Learn More -

HorizontalDimensionality Reduction in DataRobot Using t-SNE

t-SNE (t-Distributed Stochastic Neighbor Embedding) is a powerful technique for dimensionality reduction that can effectively visualize high-dimensional data in a lower-dimensional space.

Learn More